What is a section 368 Reorganization

David Ramirez

Published Apr 22, 2026

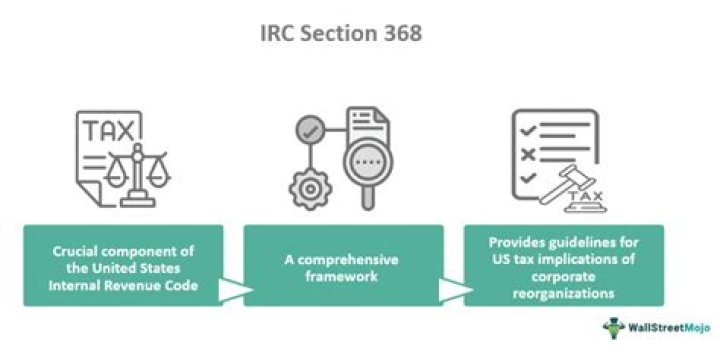

Internal Revenue Code (IRC) Section 368 allows merger and acquisition transactions to qualify as a reorganization when an acquiring corporation gives a substantial amount of its own stock as consideration to the acquired (or “target”) corporation.

What is a 368?

Overview and Fundamentals of Section 368. Section 368(A)(1) outlines a format for US tax treatment of corporate reorganizations, as described in the Internal Revenue Code of 1986. … To qualify as a tax-free reorganization, a transaction must meet the statutory requirements for one of the types of tax-free reorganizations …

How does a tax free reorganization work?

A target shareholder who receives boot in a type A reorganization recognizes gain to the extent of the lesser of the boot or the gain realized upon the exchange of the stock. If other shareholders do not receive boot, they do not recognize gain. Thus, the transaction is still termed tax-free.

What is a reorganization tax?

As a general rule, the sale of assets or stock usually results in a taxable transaction to corporations. However, reorganizations create ways for entities to limit or reduce tax liabilities simply by restructuring the overall transaction. Tax free reorganizations should not be confused with eliminating tax entirely.What is a 368 A 1 F reorganization?

Sec. 368(a)(1)(F) provides that an F reorganization is a mere change in identity, form, or place of organization of one corporation, however effected. … The underlying goal is to ensure that only one continuing corporation is involved and that the transaction is not acquisitive or divisive in nature.

How long is a DD Form 368 valid?

DD Form 368 expiration date is six months from the date of approval, so the applicant’s plans should be aligned within the given time period. In some cases, an additional three months may be granted if an extension is required.

What is a Type E Reorganization?

The “E” reorganization is defined as a re-capitalization – the exchanges of stock and securities for new stock and/or securities by the corporation’s shareholders. … In such case, there is a deemed transfer from the old corporation to the new corporation.

What is a Type B reorganization?

A type B reorganization as defined in Sec. 368(a)(1)(B) occurs when a parent corporation or its controlled subsidiary acquires the stock of a target corporation solely in exchange for voting stock of the parent corporation.What is an A reorganization?

A Type A reorganization. allows the buyer to use either voting stock or nonvoting stock. An individual who owns stock in a company is called a shareholder and is eligible to claim part of the company’s residual assets and earnings (should the company ever be dissolved).

What is AG reorganization?A Type G reorganization involves bankruptcy by allowing the transfer of a failing company’s assets to a new corporation. The controlled corporation’s stock and securities will be distributed to the former company’s shareholders under the rules for distribution that apply to Type D transfers.

Article first time published onHow do we get deferrals under Section 368?

To qualify for the tax-deferral treatment provided by Section 368, four different conditions must be met. These conditions are continuity of ownership interest, continuity of business enterprise, valid business purpose and the step transaction doctrine.

What is a Type F reorganization?

An “F” reorganization is a type of tax-free reorganization under Internal Revenue Code Section 368(a)(1)(F), which includes a mere change in identity or form of one corporation. F reorganizations are typically used to effectuate a tax-free shift of a single operating company.

How does a corporate reorganization work?

Corporate reorganization usually involves significant changes to a company’s equity base, such as: Conversion of outstanding shares to common stock. Reverse splits. The combination of the company’s shares that are outstanding to reduce the number of available shares.

Does a QSub file a tax return?

There is no separate federal income tax return for a QSub. Its operations are reported in the S corporation’s federal income tax return, thus providing a de facto consolidated return for the S corporation and its QSub.

Do disregarded entities file tax returns?

Does a Disregarded Entity Have to File Tax Returns? Since the owner pays the disregarded entity’s federal taxes on their personal return, the disregarded entity is not required to file a federal income tax return.

How do I report a merger on my taxes?

A reporting corporation must file Form 8806 to report an acquisition of control or a substantial change in the capital structure of a domestic corporation. The reporting corporation or any shareholder is required to recognize gain (if any) under section 367(a) and the related regulations as a result of the transaction.

What is an upstream C reorganization?

An upstream C with a drop is a tax-free upstream Sec. 368(a)(1)(C) reorganization of a subsidiary’s assets (an upstream C), followed by a tax-free contribution of some of the subsidiary’s assets to a new corporation (a drop). The assets not reincorporated are left in the parent corporation’s hands.

What is a 351 transaction?

351 allows a tax-free incorporation transfer if certain requirements are met, including that the property must be transferred to a corporation by one or more persons in exchange for stock in the corporation, and, immediately after the exchange, the transferor(s) is (are) in control (as defined in Sec.

What are tax-free transactions?

This type of transaction is deemed to be “tax-free” because the parent company is still able to divest the business it wants to separate from, but the company does not incur capital gains tax on the divestiture, which would be the case in an outright sale of the business unit to another company.

What is a DD Form 368 used for?

Initiating Agencies (recruiters) will use DD Form 368, Request for Conditional Release from the Reserve or Guard Component, for authorization to transfer Airmen between Reserve and Regular Components of the Military Services (Inter-service Transfer), with the exception of those requesting transfer to the Air Force …

How long does a DD 368 take to process?

The total process should take no more than 90 days from the day you submit your completed packet to your Unit.

Can you switch from army to air force while under contract?

Unless you are a medical officer, you cannot change from army to air force. However, it is possible that you may be posted on deputation to an IAF unit.

What is another word for reorganization?

In this page you can discover 13 synonyms, antonyms, idiomatic expressions, and related words for reorganization, like: restructuring, change, improvement, readjustment, , reconstitution, , reorganisation, rearrangement, reestablishment and shakeup.

What are the main types of corporate reorganization?

- Mergers and consolidations. A statutory merger is based on the acquisition of a company’s assets by another company, either in the same or different industry. …

- Corporate buyouts. …

- Corporate takeovers. …

- Recapitalization. …

- Divestiture (Spinoffs and split-offs)

How does section 338 election work?

It’s known as a Section 338 election. Under Sec. 338 of the Internal Revenue Code, a corporate buyer and the target company can jointly elect to treat a stock purchase/sale transaction as an asset purchase/sale transaction for federal income tax purposes. … 338 election only affects the tax treatment.

Which reorganization does not allow for any boot?

The “B” reorganization is similar to the reverse triangular merger, except that the latter allows boot, eliminates minority shareholders, and requires the buyer to acquire “substantially all” of the target’s assets.

Are mergers tax free?

The federal tax code provides for tax free mergers and acquisitions in certain situations. In tax-free mergers, the acquiring company uses its stock as a significant portion of the consideration paid to the acquired company.

Can you exchange stock for stock tax free?

Under IRC §1032, a corporation can issue stock in exchange for money or other property tax-free. Under §1036, common stock or preferred stock of the same corporation can be exchanged tax-free for stock of the same type, whether it is exchanged between the corporation and the stockholder or between stockholders.

Can an LLC do an F reorganization?

The F Reorganization can facilitate a freeze when you have an existing corporation by creating a two-tier structure where a corporation owns the preferred shares or units of a subsidiary corporation or LLC, and then new common shares or units are issued to new owners/investors in the subsidiary.

Can a C Corp do an F reorg?

While F reorganizations can also be used with C corporations, an F reorganization is particularly well suited for a variety of transactions involving S corporations. All section references herein, other than to Regulations, are to the Internal Revenue Code of 1986, as amended. Reg. § 1.368-2(m)(1).

Can an S Corp own an S Corp?

In general, corporations aren’t allowed to be shareholders. The only exception that allows an S corp to own another S corp is when one is a qualified subchapter S subsidiary, also known as a QSSS. … The original business can own the new business as an S corp if it owns all of the shares.