What is normal costing system

Victoria Simmons

Published Apr 18, 2026

Normal costing is used to derive the cost of a product. This approach applies actual direct costs to a product, as well as a standard overhead rate. … A standard overhead rate that is applied using the product’s actual usage of whatever allocation base is being used (such as direct labor hours or machine time)

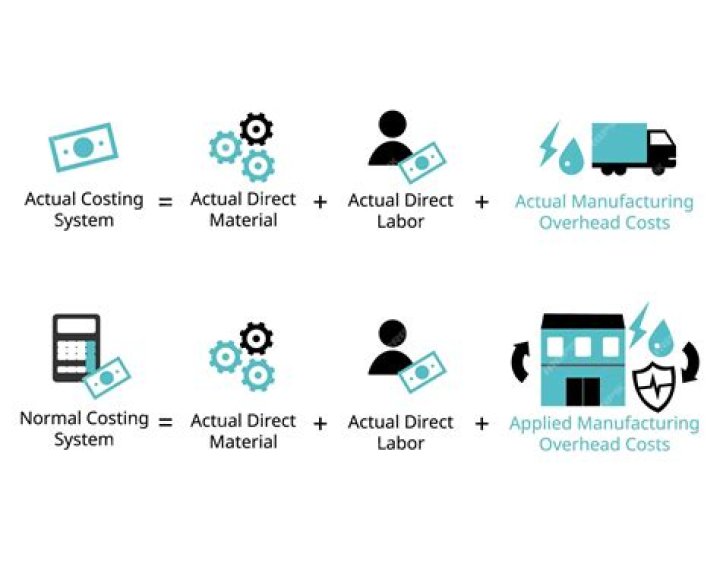

What is normal costing vs actual costing?

Actual costing uses the real expenditures that were incurred in the production of a product or service. Extended normal costing uses the actual costs of direct materials and direct labor but relies on a budgeted figure for overhead costs.

What is normal costing formula?

The Normal Costing Method For example, if Paul’s plant has $750,000 of budgeted overhead and 50,000 in budgeted labor hours, the rate is $750,000 / 50,000 = $15.00 per labor hour.

What is normal cost example?

Normal Cost are the normal or regular costs which are incurred in the normal conditions during the normal operations of the organization. They are the sum of actual direct materials cost, actual labour cost and other direct expense. Example: repairs, maintenance, salaries paid to employees.What is the costing system?

A costing system is designed to monitor the costs incurred by a business. The system is comprised of a set of forms, processes, controls, and reports that are designed to aggregate and report to management about revenues, costs, and profitability.

What is normal costing in cost accounting?

Definition: Normal costing is cost allocation method that assigns costs to products based on the materials, labor, and overhead used to produce them. In other words, it’s a way to find the price of an item that is being produced using three different cost factors (which make up the product cost).

Why do companies use normal costing?

Most companies use Normal/standard costing because to assign production cost to items, normal costing uses a fixed yearly overhead rate and gives in a more consistent and pragmatic cost driver for all units created throughout an accounting year.

What are types of costing system?

- Absorption costing. Absorption costing, sometimes referred to as full costing, is used by a company to determine all costs that go into the manufacturing of a specific product. …

- Historical costing. …

- Marginal costing. …

- Standard costing. …

- Lean costing. …

- Activity-based costing.

What is the difference between historical costing and standard costing?

Standard Cost is determined and recorded before actual performance while Historical Cost is related to the past transactions i.e. the financial transactions are recorded after the actual performance.

What is costing system with examples?Question: A process costing system is used by companies that produce similar or identical units of product in batches employing a consistent process. Examples of companies that use process costing include Chevron Corporation (petroleum products), the Wrigley Company (chewing gum), and Pittsburgh Paints (paint).

Article first time published onWhat are the two basic types of costing systems?

The two basic types of cost accounting systems are: Job order costing and process costing.

Is normal costing job costing?

Normal Costing Due to the need for immediate access to job costs, many companies use a predetermined/budgeted, manufacturing overhead rate to estimate manufacturing overhead costs. Commonly, predetermined rates may be derived from the company applying overhead costs on the basis of labor hours or machine hours.

Why might Managers at products prefer to use normal costing?

Normal costing provides managers with information at the end of a fiscal year when they know actual manufacturing overhead costs. This approach is preferable to managers to improve the company’s spending efficiency and increase overall profits.

What are the limitations of standard costing?

Three of the disadvantages that result from a business using standard costs are: Controversial materiality limits for variances. Nonreporting of certain variances. Low morale for some workers.

Which of the following are objectives of standard costing?

The objective of the standard costing and budgeting is to achieve maximum efficiency and cost control. Under both the systems actual performance is compared with predetermined standards, deviations, if any, are analysed and reported.

What is the difference between budgeted and standard cost?

Question: What is the difference between standard costs and budgeted costs? Answer: The term standard cost refers to a specific cost per unit. Budgeted cost refers to costs in total given a certain level of activity.

What are the 4 types of costing?

Direct, indirect, fixed, and variable are the 4 main kinds of cost.

What applies to a standard costing?

Standard costing is the practice of estimating the expense of a production process. It’s a branch of cost accounting that’s used by a manufacturer, for example, to plan their costs for the coming year on various expenses such as direct material, direct labor or overhead.

What are the 3 costing methods?

The main costing methods available are process costing, job costing and direct costing. Each of these methods apply to different production and decision environments.

How many costing systems are there?

There are two main cost accounting systems: the job order costing and the process costing.

Which costing system is the best?

At Terillium we usually recommend businesses in the manufacturing industry use standard costing. A standard cost system has the highest level of cost control, cost integrity, and financial stability. Standard costing measures day-to-day values of inventory and cost of goods sold against (“standard”) levels.

Who is the main user of cost accounting system?

Cost accounting provides the detailed cost information that management needs to control current operations and plan for the future. Cost accounting information is also commonly used in financial accounting, but its primary function is for use by managers to facilitate their decision-making.

Why are costing systems important to a business?

It allows management to check the raw materials in each stage of production. It helps the business to lower the cost of the business operation by identifying and controlling relevant items. … In just-in-time inventory systems, the company orders the raw material as when they need it.

What is factory burden?

Factory burden is those costs incurred in the production process, other than direct costs. These costs are accumulated into cost pools at the end of each reporting period, and then allocated to units of production. The allocated costs are eventually charged to expense when the associated units of production are sold.

How does actual costing differ from normal costing quizlet?

> The only difference between costing a job with normal costing and actual costing is that normal costing uses BUDGETED indirect-cost rates where actual costing using ACTUAL indirect-cost rates calculated annually at the end of the year. … All product costs are accumulated in the work-in-process control account.

Why might Managers at Darby products prefer to use normal costing choose all that apply?

Why might managers at Darby Products prefer to use normal costing? Normal costing enables Darby Products to use the budgeted manufacturing overhead rate determined at the beginning of the year to estimate the cost of a job as soon as the job is completed.

How do you calculate indirect cost under normal costing?

The budgeted indirect cost rate formula is calculated by dividing the budgeted annual indirect costs by the budgeted annual quantity of the cost allocation base.

Is Standard costing Still Relevant?

Therefore, standard costing can only remain relevant when used to measure the trend in performance, and ultimately give a rate of change of a company’s performance. Moreover, for it to be effective, there is a need for reviewing and making improvements so that it can be relevant to companies.

Why are standard costs important?

Standard costs are useful in setting selling prices. The budget shows the expected expenses incurred by the business. By considering these expenses, management can determine how much to charge for a product so that it can produce the desired net income.