What is deferred tax liability and asset

Nathan Sanders

Published Apr 23, 2026

A deferred tax asset is a business tax credit for future taxes, and a deferred tax liability means the business has a tax debt that will need to be paid in the future. You can think of it as paying part of your taxes in advance (deferred tax asset) or paying additional taxes at a future date (deferred tax liability).

What is the deferred tax liability?

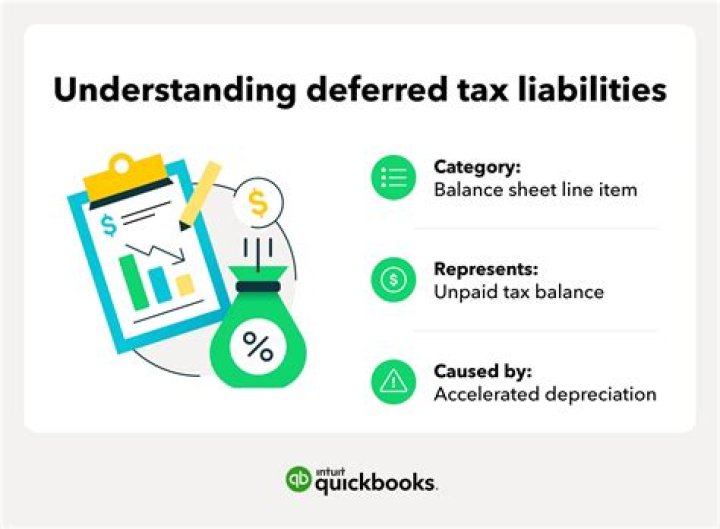

A deferred tax liability is a listing on a company’s balance sheet that records taxes that are owed but are not due to be paid until a future date. The liability is deferred due to a difference in timing between when the tax was accrued and when it is due to be paid.

Is deferred tax a current asset?

Deferred taxes are a non-current asset for accounting purposes. A current asset is any asset that will provide an economic benefit for or within one year. Deferred taxes are items on the balance sheet that arise from overpayment or advance payment of taxes, resulting in a refund later.

What causes deferred tax assets and liabilities?

As per AS 22, deferred tax assets and liability arise due to the difference between book income & taxable income and do not rise on account of tax expense itself. MAT does not give rise to any difference between book income and taxable income.What is deferred tax asset example?

One straightforward example of a deferred tax asset is the carryover of losses. If a business incurs a loss in a financial year, it usually is entitled to use that loss in order to lower its taxable income in the following years. 3 In that sense, the loss is an asset.

Is Nol a deferred tax asset?

The full loss from the first year can be carried forward on the balance sheet to the second year as a deferred tax asset.

How are deferred tax assets or liabilities calculated?

Income as per Income tax authorities In the given situation, excess tax paid today due to the difference among the income computed as per books of the company and the income computed by the income tax authorities is 12,60,000 – 12,00,000 = 60,000. This amount i.e. 60,000 will be termed as deferred tax asset (DTA).

What is deferred tax in simple terms?

IAS 12 defines a deferred tax liability as being the amount of income tax payable in future periods in respect of taxable temporary differences. So, in simple terms, deferred tax is tax that is payable in the future.What is deferred tax asset 12?

When a company overpays for a particular tax period, this can be marked as a deferred tax asset on the balance sheet. … A deferred tax asset can also occur due to losses that are carried over to a new accounting period from a previous accounting period and can then be claimed in the new period as an asset.

Is a deferred tax liability a current liability?Deferred income tax shows up as a liability on the balance sheet. … Deferred income tax can be classified as either a current or long-term liability.

Article first time published onWhen deferred tax asset is created?

Deferred tax assets originate when the amount of tax has either been paid or has been carried forward but it has still not been acknowledged in the statement of income. The actual value of the deferred tax asset is generated by comparing the book income with the taxable income.

Is deferred tax liability a current or non current liability?

The new standard requires deferred tax liabilities and assets to be classified as noncurrent in a classified statement of financial position.

How do you use deferred tax assets?

Conclusion. Deferred tax assets in the balance sheet line item on the non-current assets, which are recorded whenever the Company pays more tax. The amount under this asset is then utilized to reduce future tax liability.

How do you record deferred tax assets?

- EBITDA. read more = $50,000.

- Depreciation as per books = 30,000/3 = $10,000.

- Profit Before Tax. …

- Tax as per books = 40000*30% = $12,000.

How are deferred tax liabilities created?

In simple words, Deferred tax liabilities are created when income tax expense (income statement item) is higher than taxes payable (tax return), and the difference is expected to reverse in the future. DTL is the amount of income taxes that are payable in future periods as a result of temporary taxable differences.

Where are deferred tax assets on the balance sheet?

It is shown under the head of Non- Current Assets in the balance sheet. It is shown under the head of Non- Current Liability in the balance sheet. It is important to mention that both the deferred tax asset and deferred tax liability are created for the temporary differences only.

What is deferred asset?

A deferred asset is an expenditure that is made in advance and has not yet been consumed.

How do you calculate nolco?

Calculate the Net Operating Losses For example, if your business has a taxable income of $700,000, tax deductions of $900,000 and a corporate tax rate of 40%, its NOL would be: $700,000 – $900,000 = -$200,000. Because the business does not have taxable income, it will not be paying any taxes for the tax year.

Can you net off deferred tax assets and liabilities?

Company A also has a legally enforceable right to offset current tax assets and liabilities. The recognised deferred tax asset and deferred tax liability both relate to the same taxation authority.

Is deferred tax asset included in cash flow?

Similarly, deferred tax is a non-cash item and shall be treated accordingly in the operating activities section of the cash flow statement. … Whereas, any decrease in deferred tax asset and increase in deferred tax liability shall be added to the net profit or loss.

What is deferred tax asset in India?

1. Deferred Tax Asset. Deferred tax assets arise when the tax amount has been paid or has been carried forward but has still not been recognized in the income statement. The value of deferred tax assets is created by taking the difference between the book income and the taxable income.

Is deferred tax liability a debit or credit?

A tax deferral can be a credit — that is, a liability — if the company’s fiscal income is lower than its accounting income. In essence, the business is paying fewer income taxes in the short term, but must brace for higher income taxes in the long term.

Why does deferred tax asset decrease?

A deferred tax asset also arises from a net operating loss. When a company loses money on its operations, that loss becomes a net operating loss, which the company can hold on its books as a deferred tax asset to reduce taxable income in the future. … In this way, the write-down or write-off becomes a deferred tax asset.

Is deferred tax asset Good or bad?

Deferred tax assets bring value to every company. It is viewed as a good sign in the balance sheet of a company. It represents the taxes a company has already paid, but they are not recognised in its financial statements. It is like a pre-paid tax that helps companies to reduce their future liabilities.

How do you present deferred tax liability on a balance sheet?

30. Deferred tax assets and liabilities should be distinguished from assets and liabilities representing current tax for the period. Deferred tax assets and liabilities should be disclosed under a separate heading in the balance sheet of the enterprise, separately from current assets and current liabilities.