What is a conforming loan vs conventional

Olivia House

Published Apr 18, 2026

So in this context, the term “conventional” basically means a normal or regular loan that does not receive government backing. A conforming loan is a conventional mortgage product that meets or “conforms” to certain size limits and other parameters.

Is a conforming loan the same thing as a conventional loan?

Conforming loans are not insured or guaranteed by government agencies and, as such, are a type of conventional loan.

What is the difference between conforming and non-conforming mortgage loans?

A conforming loan meets the guidelines to be sold to either Fannie Mae or Freddie Mac, two of the largest mortgage buyers in the U.S. Non-conforming loans, on the other hand, are those that fall outside those guidelines, so they can’t be sold to Fannie Mae or Freddie Mac.

Is a conforming loan good?

A conforming loan is a mortgage that meets the dollar limits set by the Federal Housing Finance Agency (FHFA) and the funding criteria of Freddie Mac and Fannie Mae. For borrowers with excellent credit, conforming loans are advantageous due to their low interest rates.What is the downside of a conventional loan?

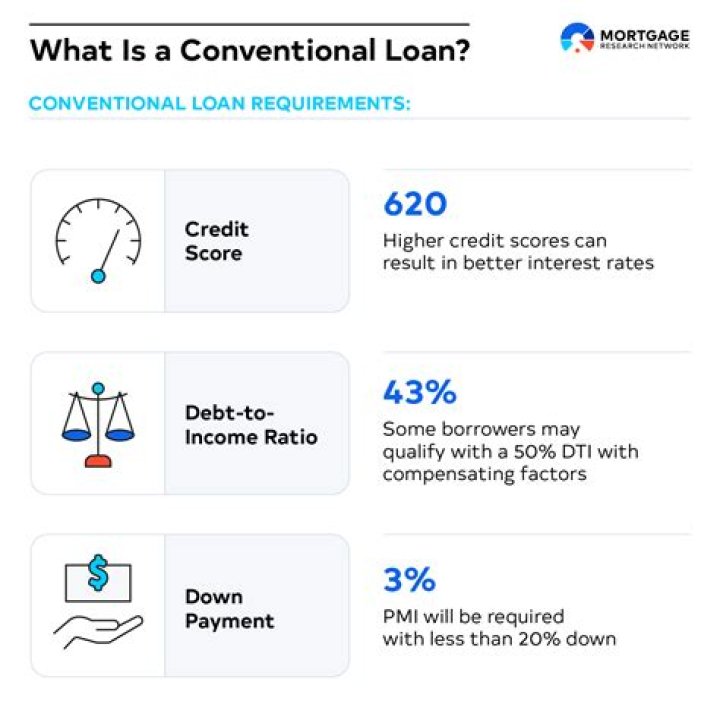

A disadvantage to conventional lending is generally lower debt-to-income ratios are required. Low income and high debt scenarios pose additional risk to private lenders, therefore debt ratio requirements are more stringent with conventional loans.

Is a conforming loan an FHA loan?

An FHA conforming loan would be at or under the FHA loan limit for that area. Furthermore, FHA home loan limits are influenced by the limits set by Fannie Mae and Freddie Mac. … FHA mortgage loan limits are not set by Fannie and Freddie, but are influenced by them.

What does 30 year fixed rate conforming mean?

A “fixed-rate” mortgage comes with an interest rate that won’t change for the life of your home loan. A “conventional” (conforming) mortgage is a loan that conforms to established guidelines for the size of the loan and your financial situation. … Terms of these conventional loans typically range from 10 to 30 years.

What is a conforming loan amount?

The conforming loan limit is the dollar cap on the size of a mortgage that Freddie Mac and Fannie Mae are willing to buy or guarantee. Mortgages that meet the support requirements by the two agencies are known as conforming loans. … The conforming loan limit for 2022 is $647,200.Who buys non conforming loans?

While there are private financial companies who will buy, package, and resell an MBS, Fannie and Freddie are the two largest purchasers. Banks use the money from the sales of mortgages to invest in offering new loans, at the current interest rate.

Is Freddie Mac a Fannie Mae?Though both enterprises are better known by their nicknames, Fannie Mae and Freddie Mac have more official titles: Fannie Mae is the Federal National Mortgage Association (FNMA) and Freddie Mac is the Federal Home Loan Mortgage Corporation (FMCC).

Article first time published onDo conforming loans have higher interest rates?

Because there is a larger secondary market for conforming loans, they often have lower interest rates — and that can mean lower monthly payments and less money spent over the lifetime of the loan.

What is the minimum down payment for a conforming loan?

Conventional loan down payment requirements The minimum down payment required for a conventional mortgage is 3%, but borrowers with lower credit scores or higher debt-to-income ratios may be required to put down more.

Are conventional loans federally backed?

Conventional loans aren’t insured or guaranteed by a government agency, they’re insured by private lenders. You need to have a higher credit score, lower debt-to-income (DTI) ratio and down payment to qualify.

Can I put 3 down on a conventional loan?

Yes! The conventional 97 program allows 3% down and is offered by many lenders. Fannie Mae’s HomeReady loan and Freddie Mac’s Home Possible loan also allow 3% down with extra flexibility for income and credit qualification.

Why do sellers want conventional loans?

Length of Time to Close. By and large, conventional loans simply tend to close faster. Less paperwork and fewer stipulations allow these mortgages to be processed more quickly, and many sellers find this to be an attractive bonus.

Is Conventional better than FHA?

FHA loans allow lower credit scores than conventional mortgages do, and are easier to qualify for. Conventional loans allow slightly lower down payments. … FHA loans are insured by the Federal Housing Administration, and conventional mortgages aren’t insured by a federal agency.

Is 3.25 A good mortgage rate?

However, rates are rising, and homeowners who can lock in between 3 and 3.25 percent are still in a great position. In a historical context, 3.25 percent is an ultra–low mortgage rate.

What is a good interest rate on a conventional loan?

Loan typeAverage Interest RateAPRConventional 15-Year FRM3.125%3.125%Conventional 5/1 ARM3%2.868%

What type of home loan has the lowest interest rate?

What type of home loan has the lowest interest rate? VA loans typically have the lowest interest rates. However, the VA program is only available to eligible service members and veterans. For non-VA buyers with strong credit, a conventional loan will typically offer the lowest rates.

Is Fannie Mae better than FHA?

The difference between a FHA and Fannie Mae loans are that the FHA insured loan is a loan by The US Federal Housing Administration mortgage insurance backed mortgage loan that is provided by a approved lender. … The Fannie Mae loan has a higher credit score requirement at 620 to 640 which is higher than the FHA loan.

What does conforming fixed rate mean?

When your loan amount meets federal guidelines for conventional financing, your loan is considered “conforming.” If your loan’s interest rate will not change at any time during the repayment term, it’s consider “fixed.” Conforming fixed loans are common mortgage programs. …

What are examples of GSE?

- Federal National Mortgage Association (FNMA or Fannie Mae)

- Federal Home Loan Mortgage Corporation (FHLMC or Freddie Mac)

- Federal Agricultural Mortgage Corporation (Farmer Mac)

What are examples of non-conforming loans?

Non-conforming loans are loans that do not conform to the guidelines of Fannie Mae or Freddie Mac. The most common types of non-conforming loans are government-backed mortgages – like FHA, USDA and VA loans – and jumbo loans that are above Fannie Mae and Freddie Mac limits.

Are jumbo loan rates higher than conventional?

Taking out a jumbo mortgage doesn’t immediately mean higher interest rates. In fact, jumbo mortgage rates are often competitive and may be lower than conforming mortgage rates. … But, if lenders are able to provide jumbo mortgages, they’ll usually keep their rates competitive.

Does conforming loan limit include down payment?

The upfront cost alone can be prohibitive for many borrowers. While conforming loans allow down payments as low as 3%, most jumbo loan borrowers are required to put down a minimum of 20%. They’ll also need to have a credit score in the 700s and a DTI of 45% or lower to qualify.

What is a conforming loan 2021?

– The Federal Housing Finance Agency (FHFA) today announced the conforming loan limits (CLLs) for mortgages to be acquired by Fannie Mae and Freddie Mac (the Enterprises) in 2022. In most of the U.S., the 2022 CLL for one-unit properties will be $647,200, an increase of $98,950 from $548,250 in 2021.

Will the conforming loan limit increase in 2021?

Conforming Loan Limits Increase By 18% in 2021 for the Year Ahead.

Who is Quicken loans backed by?

About 95 percent of all Quicken’s mortgages have explicit government backing through Fannie Mae, Freddie Mac, Ginnie Mae or the Federal Housing Administration, which generally insure loans against homeowner defaults.

Do all mortgages go through Fannie Mae?

Fannie Mae is happy to buy mortgages from lenders — but not every mortgage. For Fannie Mae and Freddie Mac to be able to re-sell loans, they need to be considered safe investments. That means each mortgage must meet certain requirements or “guidelines.” Fannie Mae guidelines run more than 1,200 pages.

How do I know if my mortgage is Fannie or Freddie?

You may contact your servicer (often your bank or lender) to verify that your mortgage loan is owned or guaranteed by Fannie Mae or Freddie Mac, or you may verify it yourself by accessing the Making Home Affordable website.

What does Nmls stand for?

The NMLS Unique Identifier is the number permanently assigned by the Nationwide Mortgage Licensing System & Registry (NMLS) for each company, branch, and individual that maintains a single account on NMLS.